In the third instalment of a series of articles on COVID-19 and its implications for logistics real estate, Prologis identifies concrete learnings from its operations in China and its proprietary data globally.

In China, activity is picking up across Prologis’ business and amongst its customers, and signs are emerging of an economic recovery as many return to work. In the U.S., Prologis’ proprietary Industrial Business Indicator (IBI), which tracks customer activity in the U.S., indicates a slowdown, albeit not as deep as during the global financial crisis. In previous COVID-19 updates (March 12, March 19), the developer identified potential factors that could help temper the downturn for logistics real estate. This week, Prologis’ survey reveals that utilization rates remain elevated in mid-84% range, modestly below the 85-87% range of the last four years. This new data point indicates facilities’ continuing limited capacity to flex in order to accommodate growth where needed.

As China begins to emerge from the outbreak, Prologis’ research identifies four key metrics that could apply to both the U.S. and Europe in the coming months:

- Continued operations. Throughout the outbreak, logistics operations continued except where strict government lockdowns were mandated. For those that remained open, Prologis customers took a raft of measures to ensure safety within the facilities and undertook remedial efforts where needed. Delays in logistics real estate construction were more widespread and restarting projects has taken longer.

- A reacceleration for e-commerce. Activity was most resilient among customers focused on end consumption and city distribution, especially for e-commerce customers. Overall, deliveries continued without major disruption even in the face of labour shortages. By contrast, automotive has been less active. As in the U.S. and Europe, multiple online segments performed well, led by grocery and general retailers.

- Leases signed. Despite lockdowns and travel restrictions that limited showings during the worst point of the outbreak, activity continued (albeit at a slower pace). In February and March, Prologis signed more than a half dozen new and renewal leases in China amounting to roughly 600,000 square feet.

- Economic recovery. A sharp correction occurred in January and February. While early, an economic recovery is beginning to emerge in China as factories reopen and city life normalizes (although with prudent precautionary measures for safety). At the same time, the market remains vigilant on a second COVID-19 wave, and economic volatility still could depress logistics real estate demand in the near term.

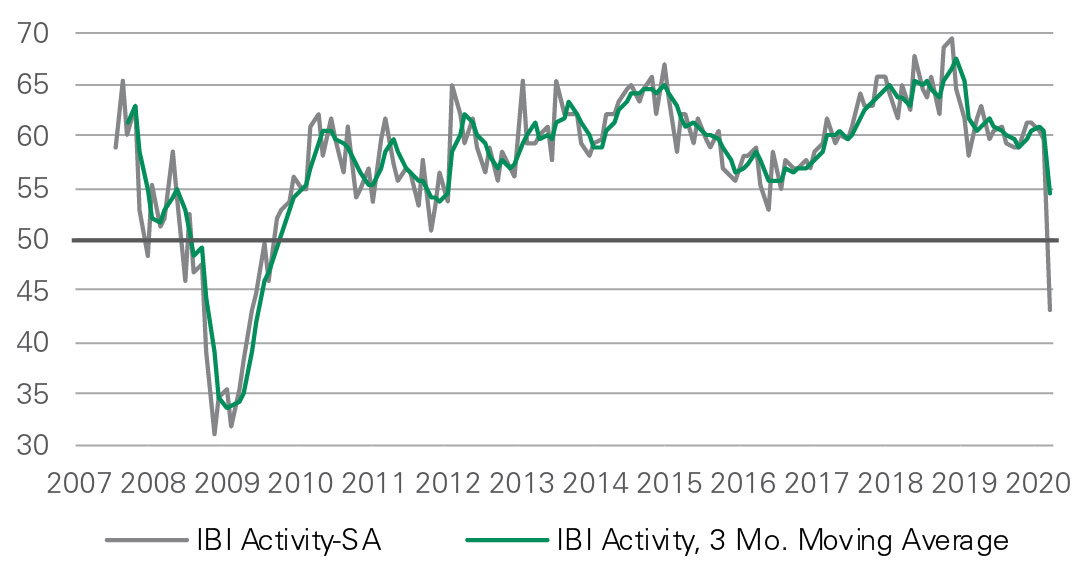

Logistics real estate in the U.S. and Europe is likely to experience a softening in activity. Consistent with the pattern in China, economic metrics in the U.S. and Europe are showing a sharp deceleration in activity. Notably in the U.S., initial unemployment claims reached their highest-ever levels and U.S. and Europe services PMIs fell to all-time lows. Prologis’ IBI also declined in March, falling to 41.7 from 60.0. Current levels are above the lows reached during the Global Financial Crisis, when the index fell to 31.1 in November 2008. Such volatility signals a recession and that logistics demand could pause or reverse in 2H’20, if not sooner, posing a risk to market vacancy rates and rent growth. One other difference from the Global Financial Crisis is ultra-low vacancies in this cycle going into a period of uncertainty. Today, vacancies are 4.6% in the U.S. and below 4% in Europe, substantially below the mid-7%s that prevailed in 2007/2008.

This month Prologis supplemented the survey with a specific focus on the impact of COVID-19 on operations. This data reveals that a small minority (22%) report a sharp decline in activity levels due to (a) no product to distribute or (b) closures for safety purposes—both of which are likely to be transitory. By contrast, a large minority (38%) report either no change or an increase in activity. The remaining respondents report a moderate slowdown and are taking precautionary measures.

Background on the Industrial Business Indicator

This proprietary monthly survey of Prologis’ U.S. customers was introduced in 2007. They collate activity levels and use that data to estimate industry utilization (out of 100%). The activity index is Prologis’ headline figure. As a diffusion index, it is benchmarked to 50, to which they add the percentage of customers who report more activity and subtract the percentage of customers who report less activity.

As Prologis noted in last week’s update, the new structural growth drivers of higher inventory levels and a reacceleration of e-commerce may combine with four factors to temper the downturn for logistics:

- strong momentum and ultra-low market vacancies;

- diverse demand and growth among certain categories due to COVID-19, including e-commerce, groceries and home improvement despite weakness in other categories such as auto;

- inventory restocking flowing from China; and

- slowed development starts.

This week, Prologis’ data indicates that facilities continue to operate with limited capacity to flex in order to accommodate growth where needed. Utilization rates remain at a still-elevated 84.5%. Prologis expects that the short term will be dominated by depressed economic activity and limited capital availability, especially for small- and medium-sized businesses. Fiscal stimulus will help. Logistics real estate demand, occupancies and rent growth all face headwinds.

Logistics is well-positioned for the long term. Looking across all real estate property types, performance will follow on how customers/users adapt in this environment—for example, office users and their adoption of telecommuting versus coworking. For logistics real estate, momentum continues to build for new structural drivers to play a role in the medium and long term, namely higher inventory levels for business continuity purposes and a reacceleration of e-commerce from growth in both new consumer categories (seniors) and product categories (groceries).