Owners are looking carefully at their exposure to risk, especially in terms of covenant strength and government measures affecting rental payments, according to Colliers International’s CEE Investment report for Q1 2020. Residential tops the sectors due to one deal but offices (27% share) have maintained their place in the order of preference, closely followed by industrial and logistics (26% share) in Q1 2020.

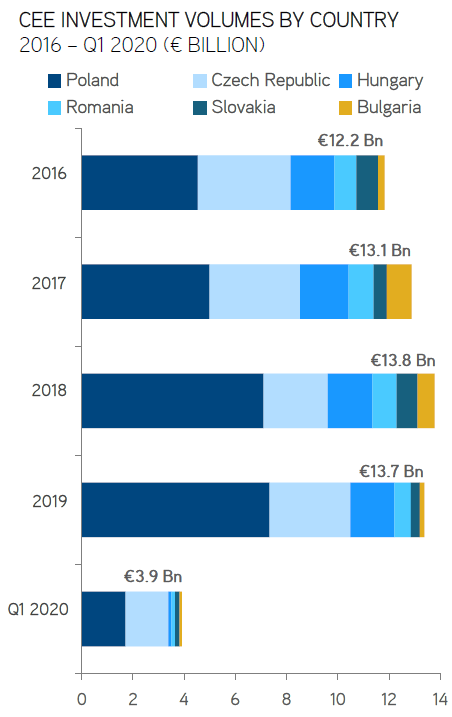

Transaction volumes were very healthy in Q1 at ca. €3.9 billion, although were supported by some deals that spilled over from 2019. As a result, Poland and the Czech Republic accounted for ca. 86% of the total volume.

Hotels and retail are the worst-hit sectors from the various lockdown measures but both had expected strong levels of activity.

Kevin Turpin, Regional Director of Research, CEE adds: “In addition to buyers, potential sellers may also decide to hold off on marketing until there is more clarity. However, owner-occupiers are quite likely to consider sale and leaseback options, if there would be a need to raise operational capital. The alternative funding option would be government-backed or alternative bank credit which may be restricted despite attractive interest rates.”

Market and pricing outlook

Many of the transactions from Q1 were already in advanced stages at the onset of the pandemic so these will not really provide the answer as this whole situation is quite unique and different from other past crises. Current owners are certainly looking very carefully at their exposure to risk, especially in terms of government measures affecting tenant rental payments and of course covenants.

It remains too early to put specific figures on any repricing due to the lack of market evidence and clarity around so many contributing factors across the various sectors. It is clear that some sectors, such as retail and hospitality, are more affected than others and Q4 2019 pricing might not be appropriate today.

This is in addition to the pre-existing challenges in these sectors thanks to the growth of e-commerce and changing consumer habits. On the other hand, we do expect high demand for logistics and subsequently some upside.

In the interests of all market players, we hope that the recent hints of positivity in terms of flattening COVID-19 case curves will continue to push through, and we can all take a fresh look at things.