The Czech logistics and industrial real estate markets are reporting new record numbers for the first half of 2022, and the records are certainly not over. Shopping centres and retail parks are also enjoying success, and many new spaces in this segment are expected to be completed in the next two years. Last but not least, the office market has also been doing well with almost 50,000 sqm of office space opened and half of it already pre-leased, while another almost 30,000 sqm will be completed this year, according to an analysis by CBRE experts.

Logistics is pulling ahead - and breaking records in the process

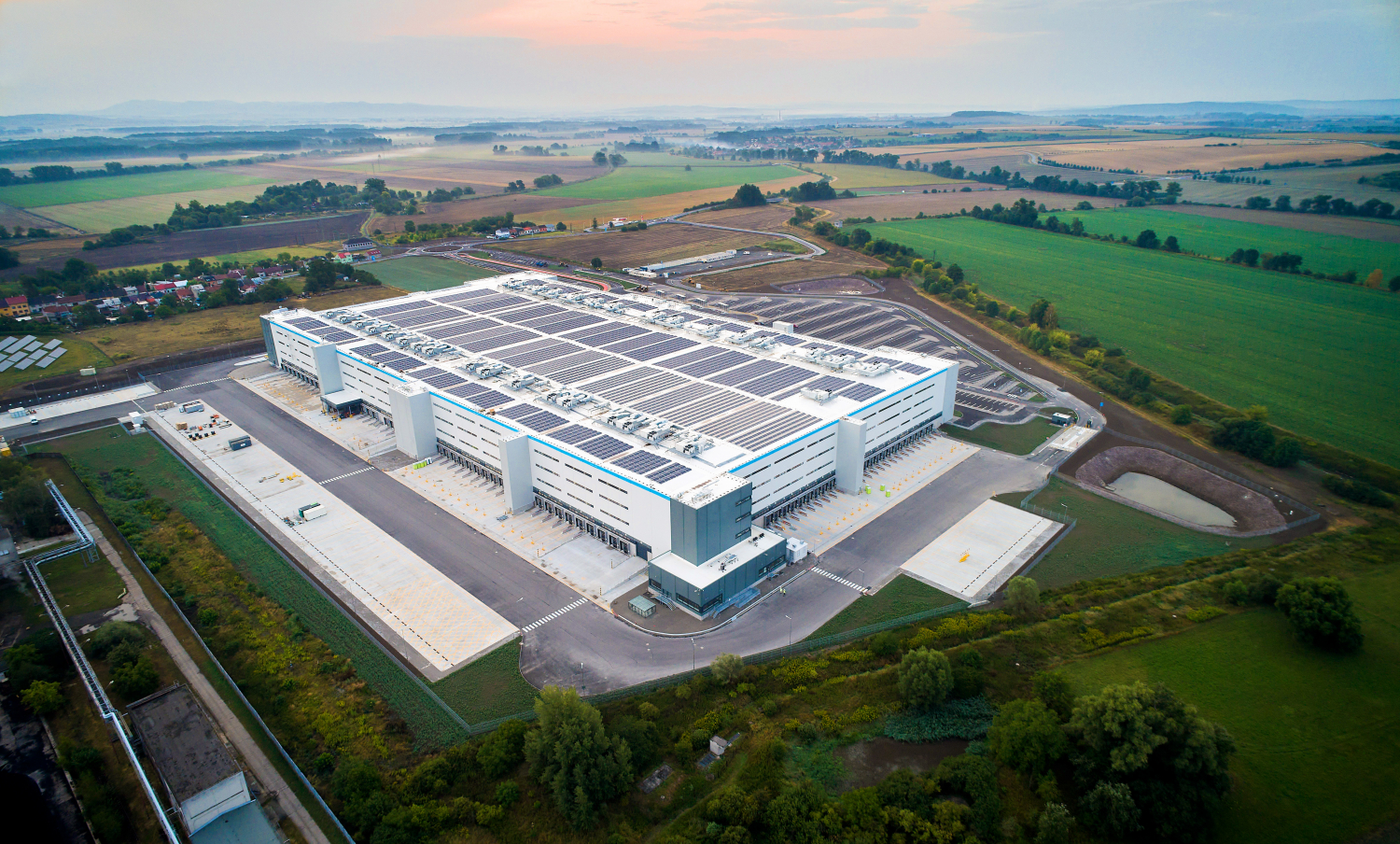

Activity in the logistics and industrial real estate market surpassed the first half of 2022 expectations: 900,000 sqm were newly leased, a 33% increase year-on-year. 130 leases were signed, of which 24 were for an area of more than 10,000 sqm and 6 for more than 20,000 sqm. The main activity on the market was related to pre-leases, which accounted for 59% of all demand. CBRE expects the total volume of newly leased space to reach 1.4 million sqm by the end of the year. This will put this year's total in second place in the historical charts after last year. At the same time, international occupiers continue to re-evaluate their strategies in terms of global supply chains, which could benefit the Czech Republic in the near future.

The current vacancy rate is just 1.5% and CBRE experts do not expect a significant change in this respect in H2. Jan Hřivnacký, Head of Industrial Leasing at CBRE, comments, "Sustainability is becoming a priority for logistics tenants and is affecting current developments to a degree never seen before." At the end of June, nearly 1.3 million sqm was under construction. Around 940,000 sqm of new space is due to come onto the market by the end of the year, with speculative development accounting for just 20% of this. High demand and record low vacancy rates (combined with rising material and construction costs as well as rising inflation) have resulted in premium rents increasing by 43% year-on-year, with upward pressure on them. Newly completed space is no longer being offered below €5 per sqm per month, with rents in Prague already hitting €8. This puts the current rental growth rate in the Czech Republic among the five fastest in Europe.

Shopping centres have fallen on hard times. The market expects a recovery in investment activity and new construction

This year, 11,200 sqm will be newly added to the market - one new shopping centre (OC Javor) will be completed and Atrium Palace Pardubice will be expanded. And although several other shopping areas will open across the country in 2023 and 2024 (e.g. OC Galerie Pardubice, but there will also be an expansion of Centrum Černý Most in Prague, Šantovka in Olomouc or Varyáda in Karlovy Vary), the retail segment will see the most retail park construction in the coming period. These have been very successful during the period of Covid and this trend will continue, also due to rising inflation, along with the expansion of discount chains. The catering sector, on the other hand, will face major challenges, as it was one of the most affected segments during the lockdowns and the associated anti-poverty measures: all this has had an impact on it and may result in the closure of some establishments and thus a reduction in supply.

Following the meteoric rise of online shopping during the covid, the pace of growth will slow slightly. Even so, e-commerce has already reached another historic milestone, currently accounting for almost 20% of all retail sales globally (18% domestically). "The success of brick-and-mortar stores will largely depend on their ability to apply omnichannel strategies. This means making available to customers the widest possible range of interconnected sales channels - from the 'physical' experience in a brick-and-mortar store to digital apps and online shopping," says Jan Janáček, Head of Retail Sector and Retail Leasing at CBRE. Anyway, as far as the first half of the year is concerned, shopping centres did well. Attendance was 10% below 2019 levels, but turnover was 10% higher. Retail sales in the country are expected to grow by 2% year-on-year.

The office market is increasingly leaning towards the tenant side. Flexibility and sustainability play a major role

Demand for new office projects in attractive locations will continue to rise (up 41% y-o-y in Prague in H1), while changes in the way offices are used towards a hybrid working model will lead to a greater interest in flexible offices. According to the "EMEA Office Occupier Sentiment Survey 2022", this is due to, among other things, the desire to reduce capital expenditure by companies, to respond flexibly to current changes and the ability to enter new markets. At the same time, the gap between rents in new premium offices and B offices will also widen.

From the beginning of the year until June, 47,880 sqm of new office space has been completed in Prague (56% of which has already been pre-leased) and a further 28,800 sqm in 6 different projects will be completed by the end of December. Quite a few new and attractive office buildings are expected to come to the Prague market in 2023. This, combined with slowing demand and the fact that almost no new companies are entering the Prague market, may lead to an increase in overall vacancy next year - it is currently around 8% (8.5% in class "A" offices and 8% in class "B" offices). So even though new premium office space is no longer being offered below EUR 14.50-15 per sqm per month, the market is becoming a "tenant's market" in many locations and especially in Prague, with landlords having to come up with incentives in many projects. According to CBRE, vacancy rates in high-quality office buildings should remain lower as these buildings are increasingly popular among tenants. Simon Orr, head of tenant representation in CBRE's office leasing team, says: "The whole office sector is now revolving around hybrid working and ESG. And office developments are adapting to this - to provide a more flexible and sustainable working environment."

ESG is not only a priority for foreign investors

Buildings are responsible for producing around 40% of the world's greenhouse gases. According to CBRE's European Investor Intentions Survey from January 2022, more than two-thirds of European investors have adopted ESG criteria in their investment practices and processes. This commitment toward ESG is now becoming the 'new normal' in Europe and the importance of ESG in the real estate industry is growing significantly. Jiří Stránský, Head of the Sustainability team at CBRE, says: "The entire Czech market is trying to understand in depth what the ESG acronym stands for and what impact it has on business. The growing inclination towards the implementation of ESG principles is not only leading to a more responsible approach to the environment and the communities that live in it. In the long term, it also increases competitiveness and property values."

CBRE expects the ESG parameters to be reflected in decision-making processes across the real estate sector, from investors to developers to tenants, with the main goal of reducing the carbon footprint. All of this will have a major impact on asset selection, acquisitions and leasing.

In the first half of the year, investment transactions amounted to almost €1.16 billion. The first half of the year was relatively strong in terms of investment, with total volumes up 35% year-on-year. Traditionally, the office real estate sector led the way, accounting for 45% of all investments. The second highest volume belonged to retail real estate, which reached 34%. Industrial and logistics properties came third with an 18% share.

In general, the market has even more potential, but supply is limited by a lack of premium products due to limited construction and slow permitting processes. Therefore, the second half of the year will be slightly lower in terms of investment, with CBRE expecting the total investment volume to reach €2 billion by the end of the year, similar to last year or the year before. The supply is currently low, especially for premium properties and properties close to completion. Czech investors are taking advantage of the fact that foreign investors have cooled down somewhat in their interest and are waiting for the right premium product to appear on the market." The strong demand for investment among Czech investors continues and they already account for over half of the capital invested in the country. However, given the slow pace of new construction, some are also looking to Slovakia and Poland for assets. For others, the trend toward investing in secondary real estate is growing. In any case, Czech funds will grow in the coming years.

Investors are most attracted by industrial and logistics parks, followed by retail parks and offices. Similar interest can be expected in the second half of the year, while older properties will also be sold due to the limited supply of new buildings. The market is currently struggling with rising inflation and the search for a stable price among property owners and potential investors. CBRE anticipates that a convergence of these expectations could occur as early as the end of this year and become fully apparent early next year. Real estate yields (yields) will go up 25-75 basis points across segments during H2 2022.